Deferred Tax For Mat Calculation

How To Calculate Profit Or Loss From Balance Sheet Http Www Svtuition Org 2014 11 How To Calculate Profi Accounting Education Learn Accounting Balance Sheet

Trusts Infographic Wealth Management Financial Advice

Guide To Minimum Alternate Tax For Ind As Compliant Companies

Tax Reconciliation Under Ias 12 Example Ifrsbox Making Ifrs Easy

Deferred Tax Detailed Analysis With 5 Examples Of Accounting Entries

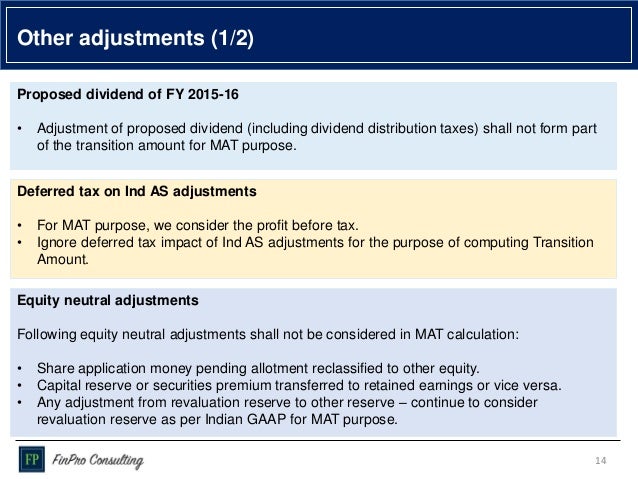

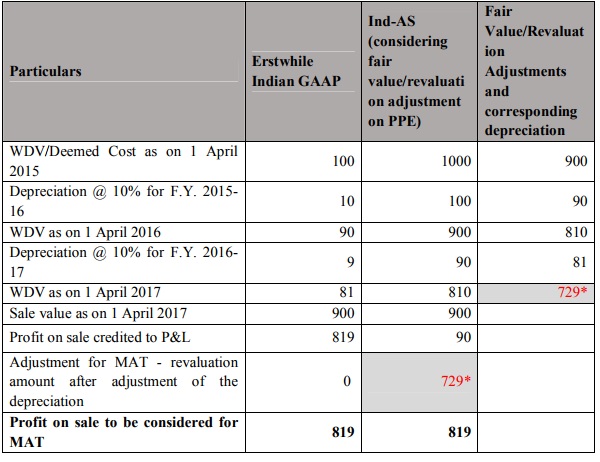

Proposed Computation Of Mat For Ind As Compliant Companies Taxing Tax

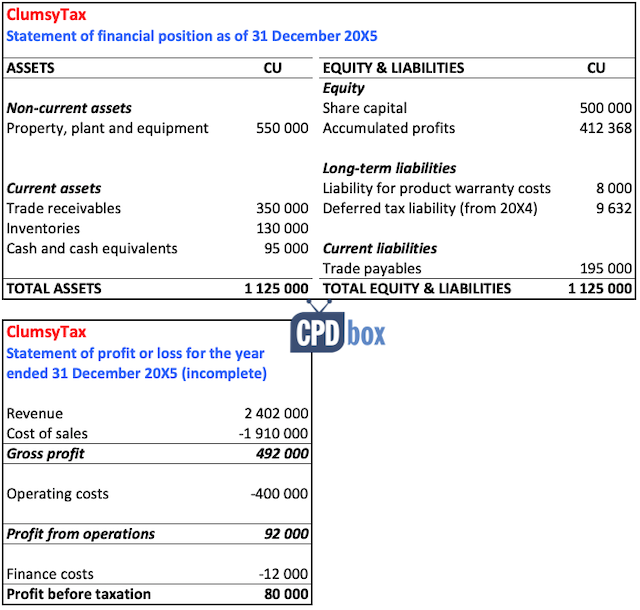

450000 then accounting profit will differ from it profit.

Deferred tax for mat calculation.

Ca Final Question Bank Dt Minimum Alternate Tax Mat

Trusts Infographic Wealth Management Financial Advice

Ind As And Mat Provisions Sec 115 Jb Of Income Tax Act

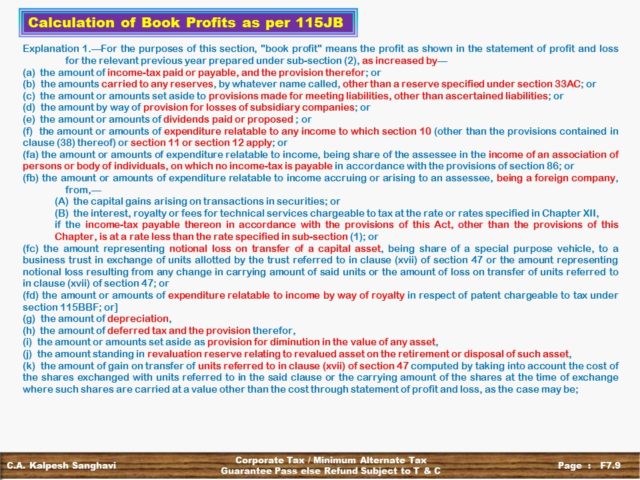

Calculation Of Book Profits For Mat Minimum Alternate Tax Section 115jb

Calculation Of Mat Credit Applicability Of Minimum Alternate Tax

Cbdt Circular Of Clarifications Faqs On Computation Of S 115jb Book Profit For Ind As Useful Miscellania

Deferred Tax Liability Accounting Double Entry Bookkeeping

Book Profit Definition Examples How To Calculate Book Profit

Calculation Of Book Profits For The Purpose Of Mat Section 115jb

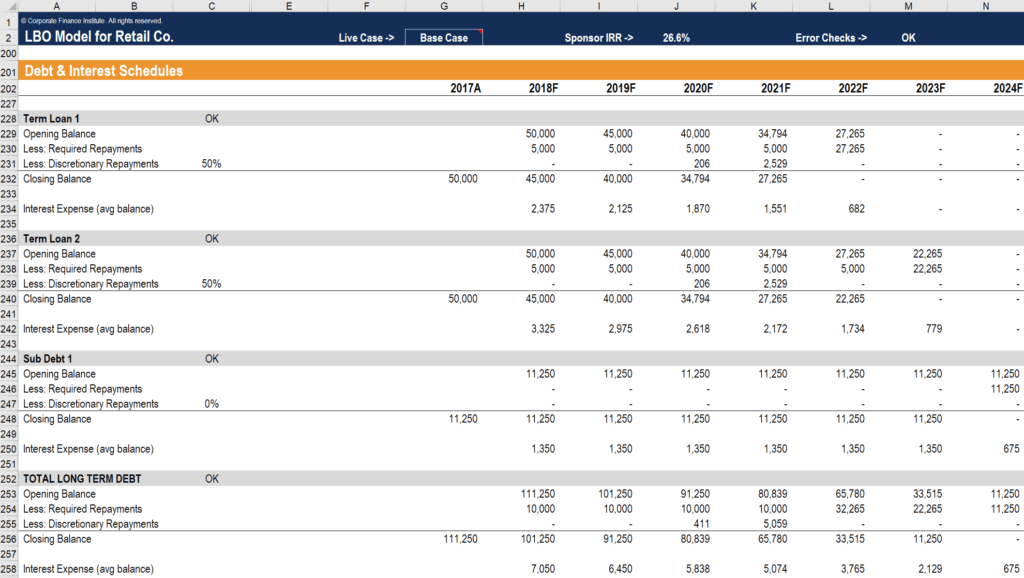

Debt Schedule Timing Of Repayment Interest And Debt Balances

Tax Guide For Rental Investments Side 1 Tax Guide Investing Rental

Deferred Tax Asset Or Liability Its Treatment In Books Of Accounts

Minimum Alternate Tax Or Mat With Detailed Understanding

Taxation Assessment Town Of The Blue Mountains On

Section 115baa And 115bab New Tax Rate For Companies

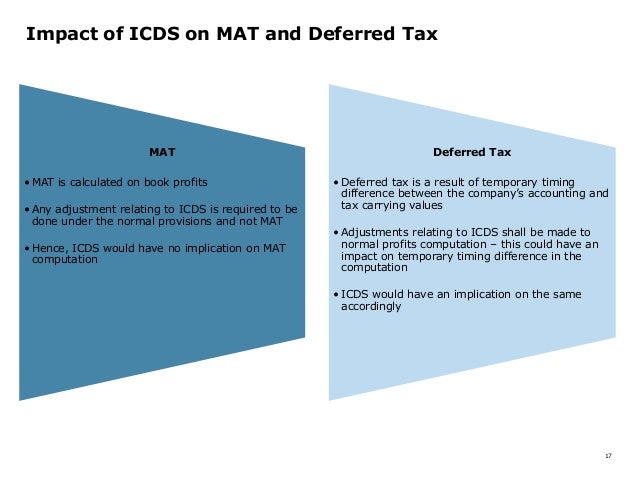

Session On Icds I To X Sandeep Jhunjhunwala

Entries Archive Strategic Finance

Https Www2 Deloitte Com Content Dam Deloitte In Documents Tax In Tax Minimum Alternate Companies Noexp Pdf

1

Firms Need To Evaluate Feasibility Of Opting Lower Corporate Tax Rates The Financial Express

Http Windsormachines Com Wp Content Uploads 2019 08 Subsidiary Financials 2018 19 Pdf

All About Deferred Tax And Its Entry In Books

Is Education Cess On Income Tax A Deductible Expenditure Under Section 40 A Ii

Http Windsormachines Com Wp Content Uploads 2018 08 Financials Subsidiaries Wml Pdf

Source : pinterest.com